Smart home is a smart system that anticipates and responds with intuitive and at times automated control of some or all of the amenities in a home that include TV, lighting, music, safety & security, climate, energy & water, and more. The smart home technology has grown tremendously since 2010 and transitioned from wired technology to wireless technology with emergence of wireless technologies, such as Bluetooth, Wi-Fi, and mobile Internet. The Internet of Things (IoT) has enabled the rapid growth of smart homes, connecting physical devices with internet connectivity and sensors providing new services to households. The trend of smart home is shifting towards the centralized control. For example, Amazon Echo and Google Home are heading in the direction of centralized smart home control.

The smart home market has reached to about USD 150 billion by 2025 and is expected to grow at 12.9% annually through from 2020-2025. This growth is expected to be driven by the factors, such as considerable growth of IoT market, improving energy efficiency, and increasing demand for security devices. A major factor restraining the growth of this market is the security issues over internet. Favorable government regulations are being implemented in several countries across the globe and next generation technologies, such as 3D gesture-based remote control in the home entertainment will present huge opportunities for smart home market.

The market for entertainment and other controls has accounted for the largest share of the smart home market in 2017, attributed to the high penetration rate of products such as smart meters and smoke detectors. Although the increasing cost of electricity is a major concern for household consumers, the market for energy saving devices will have a higher demand through 2023. Changing lifestyles and rising purchasing power of people are also expected to drive the market for smart home products worldwide. The market for lighting control is expected to grow at a higher rate because these smart home products are aimed at reducing electricity consumption in homes during the day.

The software and services pertaining to smart homes has been growing at a considerable rate as it enables users to control systems and devices installed in their homes. Most of the devices/systems, such as lighting control, HVAC control, security and access control, entertainment control, smart kitchen, and smart home appliances can be accessed and controlled using smartphones, computers, tablets, laptops, and hubs as these are enabled by the compatible software solutions and algorithms designed by smart home providers. Vivint, Inc. (US.), Comcast Corporation (US), The ADT Corporation (US), GE Healthcare (UK), AT&T, Inc. (US), Siemens Healthcare (Germany), Opower (US) and Time Warner Cable (US) are some of the major players that provide software solutions and services for smart homes.

North America accounted for the major market in 2017, accounting for ~45% of the global smart home market. However, the rising number of new residential projects and the increasing initiatives to strengthen the building infrastructure and increased focus on smart homes and smart cities is expected to make Asia-Pacific a potential market through 2023. The demand for energy saving products in Europe is also an important market for smart homes, as this region has been majorly focusing on energy savings.

Some of the major players in the smart home market include Siemens AG (Germany), General Electric Company (US), Johnson Controls, Inc. (US), Schneider Electric (France), ABB Ltd. (Switzerland), Honeywell International, Inc. (US), United Technologies Corporation (US), Ingersoll-Rand PLC (Ireland), Samsung Electronics Co., and Legrand S.A. (France).

1 Introduction

1.1 Goal & Objective

1.2 Report Coverage

1.3 Supply Side Data Modelling & Methodology

1.4 Demand Side Data Modelling & Methodology

2 Executive Summary

3 Market Outlook

3.1 Introduction

3.2 Current & Future Outlook

3.3 DROC

3.3.1 Drivers

3.3.2.1 Demand Drivers

3.3.2.2 Supply Drivers

3.3.2 Restraints

3.3.3 Opportunities

3.3.4 Challenges

3.4 Market Entry Matrix

3.5 Market Opportunity Analysis

3.6 Market Regulations

3.7 Pricing Mix

3.8 Key Customers

3.9 Value Chain & Ecosystem

4 Market Demand Analysis

4.1 Smart Home Market, Protocols and Technologies

4.2 Protocols & Standards

4.2.1 Digital Addressable Lighting Interface (DALI)

4.2.2 KNX

4.2.3 Modbus

4.2.4 Building Automation and Control Network (BACNet)

4.2.5 Black Box

4.2.6 Power Line Communication (PLC)

4.2.7 Digital Multiplexer (DMX)

4.2.8 Lonworks

4.2.9 Ethernet

4.3 Cellular Network Technologies

4.3.1 4G&5G Network

4.3.2 GSM (Global System for Mobile communication)/HSPA Networks

4.3.3 Code-division multiple access (Cdma) Networks

4.4 Wireless Communication Technologies

4.4.1 ZigBee

4.4.2 Z-Wave

4.4.3 Enocean

4.4.4 Wi-Fi

4.4.5 Bluetooth

4.4.6 Thread

4.4.7 Infrared

5 Smart Home Market, By Application

5.1 By Product

5.2 Lightning Controls

5.2.1 Relays

5.2.2 Timers

5.2.3 Occupancy Sensors

5.2.4 Daylight Sensors

5.2.5 Dimmers

5.2.6 Switches

5.2.7 Accessories and Other Products

5.3 HVAC Control

5.3.1 By Product

5.3.1.1 Smart Thermostats

5.3.1.2 Sensors

5.3.1.3 Control Valves

5.3.1.4 Heating and Cooling Coils

5.3.1.5 Pumps & Fans

5.3.1.6 Smart Vents

5.4 Security and Access Control

5.4.1 Security Control, By Product

5.4.1.1 Video Surveillance

5.4.1.2 Video Analytics

5.4.1.3 Security Cameras

5.4.1.4 Monitors

5.4.1.5 Storage Devices

5.4.1.6 Hardware

5.4.1.7 Accessories

5.4.1.8 Services

5.4.2 Access Control

5.4.2.1 Iris Recognition

5.4.2.2 Facial Recognition

5.4.2.3 Biometric Access Control

5.4.2.4 Fingerprint Recognition

5.4.2.5 Others

5.4.2.6 Non-Biometric Access Control

5.4.3 Smart Kitchen

5.4.3.1 Smart Cooktops

5.4.3.2 Smart Pressure Cookers

5.4.3.3 Smart Kettles

5.4.3.4 Smart Fridges

5.4.3.5 Smart Coffee Machine/ Coffee Makers

5.4.3.6 Smart Dishwashers

5.4.3.7 Smart Microwave

5.4.4 Smart Appliances

5.4.4.1 Smart Water Heaters

5.4.4.2 Smart Washers

5.4.4.3 Smart Dryers

5.4.4.4 Smart Vacuum

5.4.4.5 Smart AC's

5.4.4.6 Smart Deep Freezer

5.4.4.7 Smart Air-Purifiers

5.4.4.8 Smart Door Bell

5.4.5 Entertainment and Other Controls

5.4.5.1 By Product

5.4.5.1.1 Audio, Volume, & Multimedia Room Controls

5.4.5.1.2 Home Theater System Controls

5.4.5.1.3 Touchscreens and Keypads

5.4.5.2 Other Controls, By Product

5.4.5.2.1 Smart Meters

5.4.5.2.2 Smart Plugs

5.4.5.2.3 Smart Hubs

5.4.5.2.4 Smart Locks

5.4.5.2.5 Smoke Detectors

6 Smart Home Market, By Software

6.1 Proactive

6.2 Behavioral

7 Smart Home Market Analysis, By Region

7.1 North America

7.1.1 U.S.

7.1.2 Canada

7.1.3 Mexico

7.2 Europe

7.2.1 Germany

7.2.2 Italy

7.2.3 France

7.2.4 UK

7.2.5 Rest of Europe

7.3 Asia Pacific

7.3.1 China

7.3.2 Japan

7.3.3 India

7.3.4 Australia

7.3.5 Rest of APAC

7.4 Middle East & Africa

7.4.1 Saudi Arabia

7.4.2 UAE

7.4.3 Rest Of MEA

7.5 South America

7.5.1 Brazil

7.5.2 Argentina

7.5.3 Rest of South America

8 Supply Market Analysis (Industrial Player Analysis)

8.1 Strategic Benchmarking

8.2 Market Share Analysis

8.3 Key Players

8.3.1 Honeywell International, Inc.

8.3.2 Ingersoll-Rand plc.

8.3.3 Johnson Controls, Inc.

8.3.4 Siemens AG

8.3.5 Honeywell International Inc.

8.3.6 ABB Ltd.

8.3.7 United Technologies Corporation

8.3.8 General Electric Company

8.3.9 Schneider Electric Se

8.3.10 Legrand S.A.

8.3.11 Samsung Electronics Co., Ltd.

8.3.12 Lutron Electronics Co., Inc.

8.3.13 Leviton Manufacturing Company, Inc.

8.3.14 Acuity Brands, Inc.

8.3.15 Vodafone Group Plc. & Others

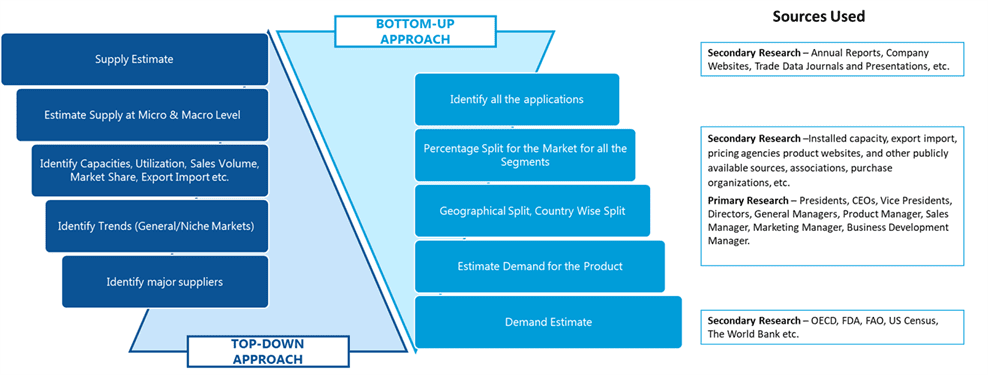

SDMR employs a three way data triangulation approach to arrive at market estimates. We use primary research, secondary research and data triangulation by top down and bottom up approach

Secondary Research:

Our research methodology involves in-depth desk research using various secondary sources. Data is gathered from association/government publications/databases, company websites, press releases, annual reports/presentations/sec filings, technical papers, journals, research papers, magazines, conferences, tradeshows, and blogs.

Key Data Points through secondary research-

Macro-economic data points

Import Export data

Identification of major market trends across various applications

Primary understanding of the industry for both the regions

Competitors analysis for the production capacities, key production sites, competitive landscape

Key customers

Production Capacity

Pricing Scenario

Cost Margin Analysis

Key Data Points through primary research-

Major factors driving the market and its end application markets

Comparative analysis and customer analysis

Regional presence

Collaborations or tie-ups

Annual Production, and sales

Profit Margins

Average Selling Price

Data Triangulation:

Data triangulation is done using top down and bottom approaches. However, to develop accurate market sizing estimations, both the methodologies are used to accurately arrive at the market size. Insert Image