The healthcare BPO market is estimated to reach USD 330 billion by 2023 growing at a CAGR of 11.0 from 2018-2023. The healthcare BPO market is primarily driven by elevating cost-saving factor, growing perception for recovery audits coupled with increasing research and development activities. However, the service reliability issue along with the complications and concerns of data privacy may hamper the growth of this market. In addition, implementation of IT in Healthcare sector serve to be the growing opportunity for healthcare BPO market. The adoption of BPO services is also responsible for propelling the growth of the market.

The healthcare BPO market can be segmented into payer services, provider services, and pharmaceutical services. The payer services can be further segmented into human resource management, claims management, Customer Relationship Management (CRM), operational/administrative management, product development, care management and provider management. The induced pressure to reduce elevating Healthcare expenditures, increasing demand of niche services, increasing demand of ICD-10 over ICD-9, adoption of automation and integrated sourcing strategies and demand and recovery audits are some of the prime factors responsible for propelling the growth of this market.

The provider services of healthcare BPO market provider is further segmented into patient enrollment and strategic planning, medical billing, medical transcription, device monitoring and revenue cycle management. On the basis of provider service, revenue cycle management is expected to grow at a steady pace during the forecast period. The growing revenue cycle management market further counts to the decreasing reimbursements in the healthcare industry, resulting in the reduction of overall Healthcare expenditure coupled with supportive government policies fuels the growth of this segment in Healthcare BPO market.

The Pharmaceutical segment of this market is further classified into manufacturing outsourcing, clinical data management, and pharmacovigilance services. Factors like increasing research and development activities, strict norms, adoption of IT in the healthcare sector, and upsurge demand in RCM plays a significant role in fueling the growth of the market. However, the lack of proper and accurate information and Communication Technology infrastructure coupled with interoperability issues and lack of domain expertise may restrict the growth of the market.

Geographically, the healthcare BPO market segmented into North America, Europe, Asia, and ROW. On the basis of geography, North America dominates this market, accounting to the growing economic growth rate and increasing Healthcare expenditure throughout this region. This further resulted in increasing investments in Technologies responsible for simplifying the healthcare systems and services that further drive the growth of this market. Moreover, the adoption of BPO services in the healthcare industry, increase in medical transcription outsourcing services and adoption of cloud-based BPOs healthcare sector are for the responsible in creating great opportunities for this market. However, the increasing doubts over the quality of services, high attrition rate, and privacy concerns and data security issues may restrict the growth of the market.

The key players operating in this industry are Accenture, Tata Consultancy Services, Genpact, Boehringer Ingelheim GmbH, Cognizant, Charles River Laboratories International Inc., Covance Inc., Infosys Limited, Lonza Group Ltd. and Quintiles Inc.

1 Introduction

2 Research Methodology

3 Executive summary

4 Premium Insights

5 Market Overview

5.1 Drivers

5.2 Restraints

5.3 Opportunities

5.4 Challenges

6 Industry Insights

7 Healthcare BPO Market, By Provider Service

7.1 Healtcare BPO provider services, by typeof services

7.1.1 Revenue cycle management

7.1.2 Patient enrollment

7.1.3 Medical coading, billing and collection services

7.1.4 Medical claims processing services

7.1.5 Medical records conversion and indexing services

7.1.6 Patient Record Management and EMR

7.1.7 Patient Care

7.1.7.1 Medical Transcription

7.1.7.2 Device Monitoring

7.1.7.3 Medical Imaging

7.1.7.4 Medical Animation

7.1.7.5 Cinical services

7.1. Other Services'

7.2 Healtcare BPO provider services, by type of facility

7.2.1 Large health systems

7.2.2 Stand alone hospitals

7.2.3 Ambulatory surgical centers and clinics

7.2.4 Physician practices

7.2.5 Diagnostic laboratories

8 Healthcare BPO Market, By Payer Services

8.1 Healtchare BPO payer services market, by type of services

8.1.1 Claims Management Services

8.1.1.1 Claims Processing and Adjudication Services

8.1.1.2 Claims Settlement Services

8.1.1.3 Claims Repricing

8.1.1.4 Claims Investigation Services

8.1.1.5 Claims Indexing Services

8.1.1.6 Fraud detection/analytics and payment integrity services

8.1.2 Integrated Front-End Services and Back-Office Operations

8.1.3 Member Management Services

8.1.4 Product Development and Business Acquisition Services

8.1.5 Provider Data Management and Credentialing

8.1.6 Care Management

8.1.7 Billing and Accounts Management Services

8.1.8 HR Services

8.1.9 Member Enrolment Billing and Eligibility Services

8.1.10 Information Management Services

8.1.11 Other Services'

8.2 Healtcare BPO payer services, by type of payer

8.2.2 Private health insurance companies

8.2.3 public/ government agencies

9 Healthcare BPO Market, By Life Sciences services

9.1 Healtchare BPO life sciences services market, by type of services

9.1.1 Research & Development

9.1.2 Manufacturing

9.1.3 Non-Clinical Services

9.1.3.1 Supply Chain Management & Logistics

9.1.3.2 Sales and Marketing Services

9.1.3.2.1 Analytics

9.1.3.2.2 Marketing Services

9.1.3.2.3 Research

9.1.3.2.4 Forecasting

9.1.3.2.5 Performance Reporting

9.1.3.3 Regulatory compliance management

9.1.3.4 Contract management

9.1.3.5 Customer management

9.1.4 Other services

9.2 Healtcare BPO life sciences services, by end user

9.2.1 Pharmaceutical and biotechnology companies

9.2.2 Research Centers

10 Healthcare Analytics Market, By Region

10.2 North America

10.1.1 US

10.1.2 Canada

Europe

10.2.1 Germany

10.3 10.2.2 UK

10.2.3 France

10.2.4 Rest of Europe

Asia

10.3.1 Japan

10.4 10.3.2 China

10.3.3 India

10.3.4 Rest of Asia

10.5 RoW

10.5.1 Pacific Countries

10.5.2 Latin America

10.5.3 Middle East and Africa

11 Competitive Landscape

12 Company profiles

13 Appendix

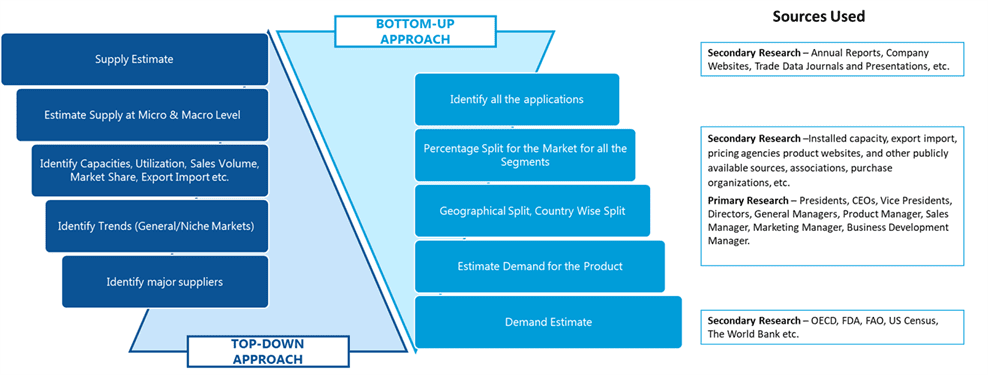

SDMR employs a three way data triangulation approach to arrive at market estimates. We use primary research, secondary research and data triangulation by top down and bottom up approach

Secondary Research:

Our research methodology involves in-depth desk research using various secondary sources. Data is gathered from association/government publications/databases, company websites, press releases, annual reports/presentations/sec filings, technical papers, journals, research papers, magazines, conferences, tradeshows, and blogs.

Key Data Points through secondary research-

Macro-economic data points

Import Export data

Identification of major market trends across various applications

Primary understanding of the industry for both the regions

Competitors analysis for the production capacities, key production sites, competitive landscape

Key customers

Production Capacity

Pricing Scenario

Cost Margin Analysis

Key Data Points through primary research-

Major factors driving the market and its end application markets

Comparative analysis and customer analysis

Regional presence

Collaborations or tie-ups

Annual Production, and sales

Profit Margins

Average Selling Price

Data Triangulation:

Data triangulation is done using top down and bottom approaches. However, to develop accurate market sizing estimations, both the methodologies are used to accurately arrive at the market size. Insert Image